Ken Rogoff Argues

Applying Bridge360 Metatheory Model lens

“The decisive risk is that the U.S. dollar system becomes progressively more expensive to stabilize, while alternative corridors become progressively more usable. … The dollar-based global operating system is not being overthrown; it is being rebalanced because its old entropy-export privilege is becoming costlier to maintain.”

I am the executive doing all the systems thinking and strategic thinking. Using my 35-year experience at the University of the Philippines, I am also the creator/developer — with help from company colleagues — of the model involved, Bridge360 Metatheory Model. LLM1, LLM2, LLM3, LLM4, and LLM5 are the rank and file clerks serving as interlocutors showing me information I have little or no time to access. [ChatGPT (LLM1), Gemini (LLM2), Perplexity (LLM3), Claude (LLM4), Grok (LLM5)]

Prompt and Zenodo links to two Bridge360 Metatheory Model monographs and marked-down algorithm files issued to LLM1, meaning ChatGPT-5.5, as pdf transcript file of Ken Rogoff Bloomberg interview on Youtube (“Is the Dollar Losing Its Luster?”) is uploaded:

“So if I look at the dynamic of how I see things unfolding, it’s that there’s this pressures from the outside that are very slow-moving, but they’re happening, to have a more multipolar system.” How does this,

resonate with Bridge360 Metatheory Model based analysis here,

https://agericomontecillodevilla.substack.com/p/global-operating-system-rebalancing (https://www.reddit.com/user/propjerry/comments/1pgnjg0/global_operating_system_rebalancing_implications/)?

Backgrounder here.

https://zenodo.org/records/17851815

https://zenodo.org/records/20020501

https://zenodo.org/records/19547281

https://zenodo.org/records/19553540

LLM1 response:

Yes. Rogoff’s formulation strongly resonates with your Bridge360-based “global operating system rebalancing” analysis. It is not merely the same topic; it is close to the same structural diagnosis, expressed in macro-financial language.

Based on the uploaded transcript, Rogoff’s key claim is: the dollar order is not collapsing overnight, but the system is undergoing slow external pressure toward multipolarity while the United States simultaneously generates internal fiscal-governance leakage through debt, political non-consensus, higher rates, and pressure on central-bank independence.

Your Substack/Reddit framing says the global economy has operated with the U.S. as the central “operating system” node: reserve currency, deepest capital markets, security guarantor, and leading technology hub; but recent developments point toward a “multi-core” arrangement involving the U.S., Europe, and Japan/East Asia Shield as differentiated load-bearing nodes. … The Reddit mirror states the same policy problem as a risk-mapping exercise: how exposed are public finances, security arrangements, supply chains, and legal systems to shifts in U.S., European, and East Asian nodes? …

Bridge360 translation

Rogoff is describing spine-corridor drift in the dollar-based global operating system.

The old spine corridor was:

U.S. fiscal capacity + Treasury liquidity + dollar invoicing + military protection + central-bank credibility + allied confidence.

His interview suggests that this corridor still exists, but its margin of navigability is narrowing. The system remains dollar-centered, but the entropy budget is no longer as generous.

In Bridge360 terms:

Rogoff’s point

Bridge360 reading

“Slow-moving pressures” toward multipolarity

Gradual perturbation of the old single-core spine corridor

China/Europe developing alternative systems

Emergence of competing or redundant corridors

U.S. debt and fiscal non-consensus

Endogenous leakage from inside the core node

Higher global interest rates

Rising entropy cost of maintaining the dollar order

Long-term dollar debt premium weakening

Collateral de-idealization; weakening of old safe-asset mythology

Short-term dollar safety still intact

Corridor not broken, but compressed into shorter time horizons

Gulf states questioning U.S. protection logic

Security-finance braid becoming unstable

Yuan/crypto/sanction-avoidance channels

Alternative settlement memes propagating under pressure

That is exactly the kind of thing Bridge360 v20.6 is designed to map: system stability is evaluated through entropy-bounded navigability, declared observer conditions, fragility limits, admissibility constraints, and stability of mappings under stress—not by assuming one permanent truth-description of the world order. (Zenodo)

The strongest resonance: external pressure + internal leakage

Rogoff’s key contribution is that he does not treat dedollarization as a simple external attack on the U.S. He sees a two-sided process:

External pressure: other states look for alternatives, especially China and Europe.

Internal pressure: the U.S. weakens its own corridor through fiscal indiscipline, debt expansion, and political inability to repair the balance sheet.

That is highly Bridge360-compatible. The decisive risk is not “China replaces the dollar tomorrow.” The decisive risk is that the U.S. dollar system becomes progressively more expensive to stabilize, while alternative corridors become progressively more usable.

So the better formulation is:

The dollar-based global operating system is not being overthrown; it is being rebalanced because its old entropy-export privilege is becoming costlier to maintain.

Why this matters for your “multi-core” thesis

Your Substack note frames the shift from a U.S.-centered global operating system toward a multi-core configuration: U.S. as still-central but politically volatile, Europe as regulatory/normative firewall, and Japan/East Asia Shield as an operational backbone for manufacturing and supply-chain resilience. …

Rogoff’s interview strengthens the U.S. node diagnosis. He gives macro-financial support to the view that the U.S. remains central but is becoming less structurally frictionless. He does not directly validate the Japan/East Asia Shield thesis; rather, he leaves space for it. His frame is currency/debt/security. Your frame is broader: currency/debt/security plus supply chains, technology, regulation, and operational continuity.

So the fit is:

Rogoff = financial-security rebalancing diagnosis.

Bridge360/Substack = generalized operating-system rebalancing diagnosis.

Band classification

This should be treated as Band B-type resonance, not Band A validation.

The Zenodo Handshake Protocol description explicitly says Bridge360 is a philosophy-of-science seeding dossier, not a completed empirical demonstration; operational thresholds, observables, perturbation protocols, and validation must be supplied by scientists, engineers, and domain specialists. (Zenodo) Likewise, v20.5 frames Bridge360 as a governance grammar requiring declared scope, perturbation limits, measurement assumptions, tripwires, audit logs, rollback semantics, and domain-specific observables. (Zenodo)

So the careful conclusion is:

Rogoff’s Bloomberg interview independently occupies the same problem-space as your Global Operating System Rebalancing note. It strengthens the plausibility of the Bridge360 diagnosis, especially the claim that the U.S.-centered financial-security corridor is becoming more fragile under combined external multipolar pressure and internal fiscal-governance leakage. But it is supporting convergence, not empirical closure.

Best concise formulation

Rogoff is saying, in ordinary macro-financial language, what Bridge360 would express as follows:

The U.S. dollar spine corridor remains dominant, but the entropy cost of preserving it is rising. External actors are slowly building alternative corridors, while internal U.S. fiscal and political dysfunction increases leakage from within the core. Multipolarity is therefore not an event but a slow reallocation of corridor-load across competing system nodes.

That is a very strong resonance with your analysis.

Prompt issued to LLM1:

This, https://zenodo.org/records/19228738 (“Global Operating System Rebalancing – Implications for Policymakers” Substack blog post)?

LLM1 response:

Yes. Zenodo 19228738 is the more directly relevant Bridge360 register for the Rogoff interview.

That Zenodo record is titled “Japan as the Early-Warning Platform” and describes itself as a Bridge360-based predictive/governance mapping for 2026–2027 systemic rebalancing, focused on the Iran-war shock, Fed transition, multi-rail finance, liquidity/collateral stress, AI-capex stress, and Japan’s role as a transmission/early-warning node. It explicitly identifies Japan as a “transmission node” and “early-warning platform” for global operating-system rebalancing, including a possible liquidity and collateral event. (Zenodo)

The Rogoff interview fits that register closely. His claim is not simply “the dollar is declining.” His claim is more precise: external slow pressures toward multipolarity are combining with internal U.S. fiscal-governance stress. In the uploaded transcript, he says outside pressures are pushing countries to look for alternatives, while inside pressures come from large U.S. debt and lack of political will to manage it. He also says higher global interest rates matter because the U.S. is the world’s biggest debtor and loses most when global rates rise.

The direct Bridge360 correspondence

Rogoff’s frame maps onto Zenodo 19228738 as follows:

Rogoff interview

Zenodo 19228738 / Bridge360 reading

“Slow-moving” pressure toward multipolarity

Multi-rail global operating-system rebalancing

Countries looking for dollar alternatives

Alternative corridor formation

China and Europe developing independent systems

Non-U.S. rails becoming operationally meaningful

U.S. fiscal problem and political non-consensus

Internal leakage from the core node

Higher global interest rates

Rising entropy cost of maintaining the U.S.-dollar spine

Weakening long-term dollar debt premium

Collateral de-idealization / safe-asset premium erosion

Gulf-state uncertainty around U.S. protection

Security-finance braid becoming unstable

Yuan, crypto, sanction-avoidance channels

Settlement-system fragmentation

So, yes: Rogoff supplies mainstream macro-financial language for the same structural process your Zenodo 19228738 register tried to formalize under Bridge360.

Why Japan matters in this mapping

Rogoff does not specifically say “Japan is the early-warning platform.” That part remains your Bridge360 inference. But his reasoning makes Japan strategically legible.

Japan sits at the intersection of:

U.S. Treasury demand;

yen-dollar funding pressures;

JGB yield normalization;

East Asian manufacturing and supply-chain continuity;

U.S. security architecture;

alternative Asian financial rails.

That is why, under the Zenodo 19228738 frame, Japan becomes a useful early-warning platform: not because Japan alone determines the global rebalancing, but because stress in the dollar-Treasury-security system is likely to show up early in Japanese rates, currency behavior, reserve positioning, and corporate/supply-chain decisions.

Strongest convergence

The strongest convergence is this:

Rogoff says the dollar system is not collapsing overnight, but its long-term privilege is being eroded by slow external multipolar pressure and internal U.S. fiscal-governance dysfunction.

Zenodo 19228738 says, in Bridge360 terms:

The global operating system is undergoing layered rewiring, with Japan functioning as an early-warning node for liquidity, collateral, energy, AI-capex, and policy-transmission stress.

Those are not identical claims, but they are structurally aligned.

Important caveat

Zenodo 19228738 classifies the material as Band C: exploratory commentary/non-certified, not settled empirical validation. (Zenodo) That is the correct discipline. Rogoff’s interview gives supporting convergence, not proof.

The upgraded assessment would be:

Rogoff’s Bloomberg interview moves Zenodo 19228738 from an isolated Bridge360 anticipatory mapping toward a stronger Band B-style resonance: a mainstream economist is now describing the same global operating-system rebalancing pressure, especially the interaction between dollar privilege, fiscal stress, long-term rates, multipolar rails, and collateral fragility. But the Japan early-warning thesis still requires empirical tracking through declared tripwires.

Prompt issued to LLM1:

This matters, https://agericomontecillodevilla.substack.com/p/cascading-global-rebalancing-and?

LLM1 response:

Yes. That Substack piece matters even more directly because it is the cascade-mechanism version of the same thesis Rogoff is now describing in macro-financial language.

Your March 6 piece says the model treats JGB instability, not merely U.S. banking or European debt, as the hidden systemic pivot point for cascading global rebalancing. It also frames the issue as thinning of high-quality collateral in overnight funding markets, with repo seizure as the plumbing mechanism and Bridge360 as the broader political-economy/system-transition framework. (Agerico Montecillo De Villa)

Rogoff’s interview then supplies the mainstream macro bridge: he says the U.S. faces external pressure from countries seeking alternatives and internal pressure from large debt, weak fiscal will, and higher global interest rates; he also notes that the long-term dollar-debt premium has weakened while short-term dollar safety remains stronger.

So the fit is very strong:

Your “cascading rebalancing” piece

Rogoff’s Bloomberg frame

Bridge360 reading

Repo collateral thinning

Long-term dollar premium weakening

Collateral de-idealization

JGB instability as hidden pivot

U.S. loses when global rates rise

Externalized entropy returns to core

Dollar system as operating-system architecture

Multipolar pressures are slow but real

Spine corridor drift

Iran/Hormuz shock as perturbation

War can accelerate dollar decline depending on outcome

Shock-driven leakage amplification

Political/electoral disorder as added entropy

Fiscal non-consensus and central-bank pressure

Governance corridor narrowing

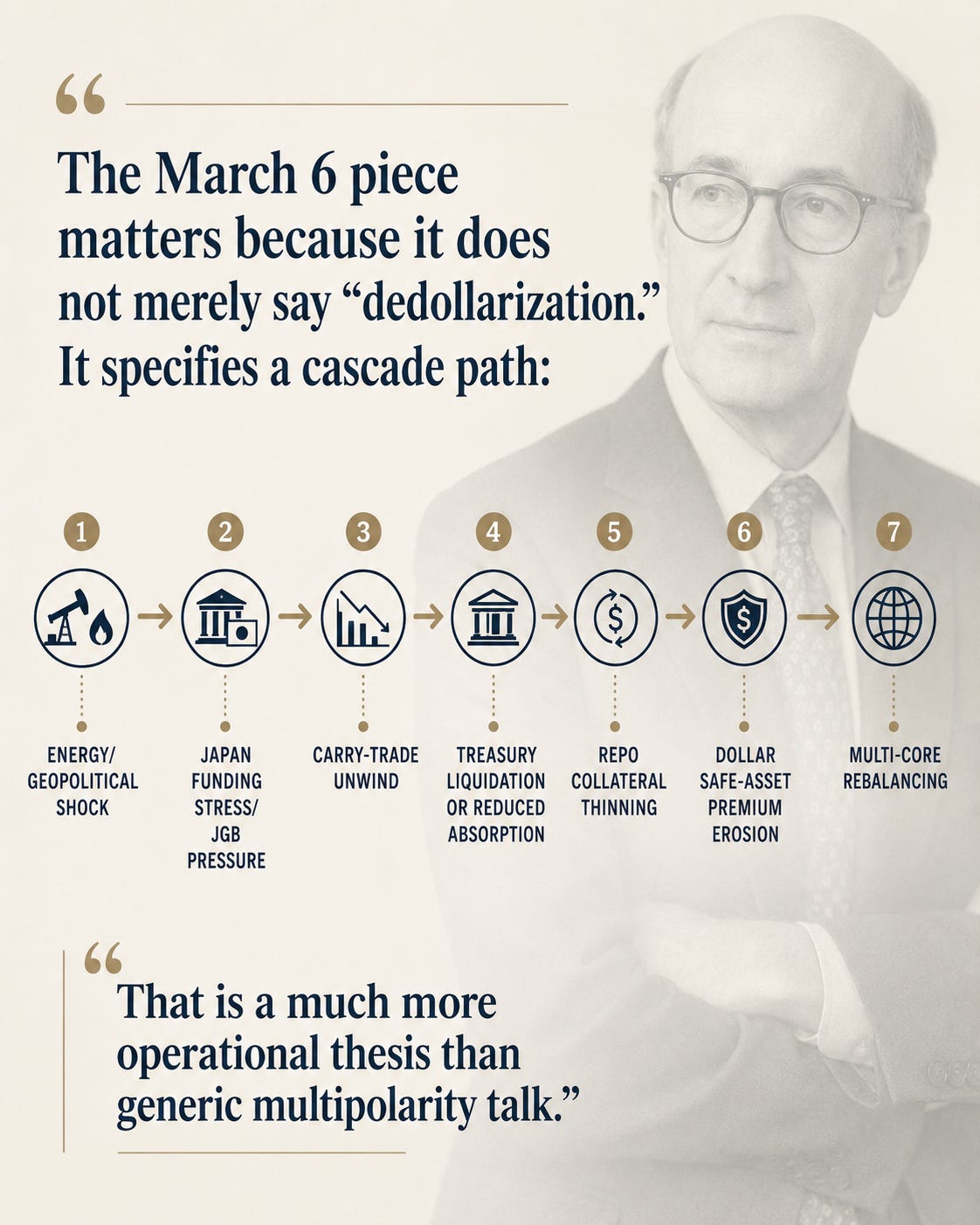

The March 6 piece matters because it does not merely say “dedollarization.” It specifies a cascade path:

energy/geopolitical shock → Japan funding stress/JGB pressure → carry-trade unwind → Treasury liquidation or reduced absorption → repo collateral thinning → dollar safe-asset premium erosion → multi-core rebalancing.

That is a much more operational thesis than generic multipolarity talk.

The current-news support is also non-trivial. Reuters reports that Iran has stopped indirect message exchanges with the U.S., that Iranian-aligned actors have discussed blocking Hormuz and Bab el-Mandeb, and that the war launched by the U.S. and Israel on February 28 has already pushed up energy prices after Iran effectively closed the Strait of Hormuz. (Reuters) That strengthens the perturbation side of your model: the energy corridor is not peripheral; it is a transmission belt into Japan, East Asia, Treasuries, and repo collateral.

The election-governance component also matters, but it must be handled carefully. The Washington Post reported a draft executive-order effort invoking alleged Chinese interference as a basis for emergency presidential power over voting, including possible restrictions on mail ballots and voting machines. (The Washington Post) Cato’s analysis says such a change would likely face swift judicial challenge and would be administratively difficult or impossible for the 2026 cycle. (Cato Institute) Bridge360-wise, the issue is not only whether such an order succeeds legally; the issue is whether the attempt itself increases perceived governance fragility at the exact moment Treasury collateral requires maximum confidence.

The weaker part of the piece is the actor-intent layer, especially the Bezos/cash-positioning thesis. It is strategically suggestive, but it should be marked as inference, not evidentiary closure. The stronger claims are structural: repo fragility, JGB transmission risk, Hormuz/energy perturbation, Fed-transition risk, fiscal non-consensus, and democratic-governance stress.

Best classification:

Band B resonance, not Band A proof.

The post matters because it anticipated a mechanism that Rogoff now describes from the dollar side: the global operating system is not simply “moving away from the dollar”; it is becoming more expensive to keep the dollar spine corridor stable. The key Bridge360 phrase would be:

The U.S.-dollar operating system remains dominant, but its collateral, fiscal, military, and legitimacy supports are thinning simultaneously; Japan/East Asia becomes an early-warning platform because stress there converts slow multipolar drift into repo-market and Treasury-collateral pressure.

That is why this piece is important. It provides the cascade architecture behind Rogoff’s “slow-moving pressures toward multipolarity.”

Use this url to view the conversation.

https://chatgpt.com/share/6a2558c8-be60-83a7-bb34-12146eed29f9

Backgrounder here.

https://zenodo.org/records/17851815

https://zenodo.org/records/20020501

https://zenodo.org/records/19547281

https://zenodo.org/records/19553540

Applying Gemini 3.1 Pro lens here.

https://gemini.google.com/share/c5478c650c2f

Applying Perplexity AI/Claude Sonnet 4.6 lens here.

https://www.perplexity.ai/search/this-makes-sense-and-is-cohere-En2DVC.dTP2qL8h_9tHBxw

Applying Grok 4.2 Expert lens here.

https://grok.com/share/c2hhcmQtNA_f808b2fa-1f28-446d-99a0-e87cd7398f36